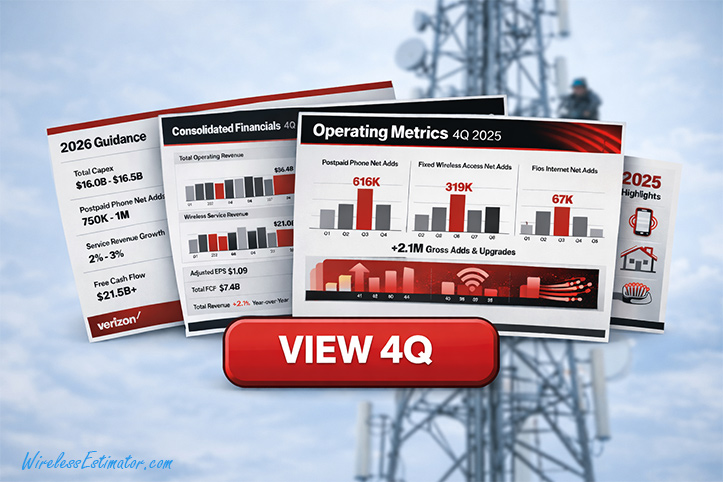

Verizon’s fourth-quarter materials underscore the carrier’s 2026 capital spending outlook of $16.0–$16.5 billion, modestly below its $17.0 billion CapEx in 2025, signaling continued but more disciplined investment in wireless and fiber infrastructure rather than a pullback from network construction.

Verizon’s fourth-quarter earnings, released Friday, delivered more than a financial beat—they offered several signals that matter directly to macro tower owners and the contractors who build, upgrade, and maintain Verizon’s network. Strong subscriber momentum, continued fiber expansion, and steady capital spending point to sustained field activity in 2026, even as the carrier maintains pressure on efficiency and cost control.

The most immediate takeaway for contractors is Verizon’s 616,000 postpaid phone net additions, its strongest quarterly performance since 2019, paired with continued growth in broadband customers. That level of subscriber expansion inevitably drives higher network utilization, which tends to surface in the field as capacity-driven site modifications, additional radio and antenna deployments, and increased RF optimization work. Growth in fixed wireless access, in particular, pushes more traffic onto existing infrastructure, increasing the likelihood of upgrades at macro sites already supporting mobile service.

Fiber continues to be a central pillar of Verizon’s strategy, reinforced by the January closing of its Frontier Communications acquisition, which significantly expands the carrier’s fiber footprint. For contractors, this means opportunity beyond traditional tower work. Fiber backhaul installations, splicing, and integration projects tied to macro sites and small-cell densification are likely to remain active, favoring firms that can operate across both wireless and wireline scopes. Contractors limited to tower-only work may find themselves competing for a smaller slice of a broader, more integrated build cycle.

CapEx Discipline Raises the Bar on Execution and Efficiency

Verizon’s capital spending outlook—roughly $16 to $16.5 billion for 2026—signals continuity rather than retrenchment. While that level of spending confirms ongoing network investment, it also underscores that projects will be scrutinized for cost, schedule, and execution discipline. For contractors, this environment rewards firms that can deliver efficiently across multiple technologies, while increasing pressure on those that rely on change orders, extended schedules, or narrow service offerings.

Maintenance and reliability are also likely to remain elevated priorities. Coming off heightened scrutiny following a nationwide outage earlier this year, Verizon has little margin for error in network performance. That typically translates into recurring field work tied to preventive maintenance, structural assessments, power systems, and resilience upgrades—areas that may not grab headlines but provide steady revenue for contractors positioned to support them.

On the earnings call, executives framed 2026 as a year of tighter execution rather than a pullback in infrastructure. CFO Anthony Skiadas said Verizon is applying “the same rigor” to capital spending “while not sacrificing” network excellence, while CEO Dan Schulman added that investment remains “focused squarely” on the company’s growth areas—language contractors will read as continued work, but with less tolerance for inefficiency or rework.

Opportunities Favor Scale and Integration, While Risks Remain for Narrow Players

There is, however, a parallel liability embedded in Verizon’s results. Management’s emphasis on efficiency and disciplined execution suggests procurement and vendor oversight will remain tight. Contractors should expect continued pressure on pricing and timelines, particularly from larger national vendors that can bundle services and absorb risk. Smaller or less diversified firms may find that access to work increasingly depends on proven performance metrics and the ability to support broader scopes.

For tower owners, Verizon’s results reinforce a familiar theme: rising network demand increases the value of well-positioned, well-maintained sites. Capacity expansions, collocations, and fiber-connected locations stand to benefit most, while sites requiring remediation or prolonged readiness work risk being bypassed in favor of faster-to-deploy alternatives.

Taken together, Verizon’s fourth-quarter performance points to continued network activity rather than contraction, but with a sharper divide between contractors that can adapt and those that cannot. The upside lies with firms that offer integrated capabilities across towers, fiber, power, and maintenance; the downside falls on those caught between rising execution expectations and tightening carrier discipline.