Facts that would have made better reading and more sense

By Ken Schmidt

After reading Wireless Estimator’s article, “Towercos tank after radical unconfirmed report of government competition,” and seeing the original article from Re/code on Friday, I felt compelled to respond. It seemed reckless to me that a website like Re/code could publish an unconfirmed report, have it copied by multiple media sources who fail to add any substantive research of their own, and as a result see over a billion dollars of market cap lost by the three public towercos and Sprint. I was glad to see Wireless Estimator do their own article condemning the Re/code article and thought that I could add my own 2 cents that might add further color (and facts) to the story.

So, is Sprint really trying to radically overhaul its network?

On Friday, the website Re/code published an unconfirmed media report that also alleges that Sprint is attempting to reduce its dependency on AT&T and Verizon’s high-speed fiber optic cables. After this article was posted, shares of American Tower (AMT), Crown Castle (CCI) and SBA Communications (SBAC), were down 3%, 6%, and 8% respectively while Sprint dropped 9%.

Here are the reasons why we think this article is just bad reporting and the selloff of the tower companies and Sprint as a result was ill-deserved. Please note that we don’t own stock or perform services for either tower company and we don’t work for Sprint (but we do have a small holding in S stock). In fact, we regularly assist landowners in negotiating cell tower leases against all 4 of these companies. However, this article uses poor inductive reasoning to come to its overall and erroneous conclusion that Sprint plans on abandoning its existing collocations on American Tower and Crown Castle towers as part of its Next Generation Network.

Perhaps it is easier to share some facts/suppositions that we know/have about Sprint’s Next Generation Network and you should be able to see how the facts can be improperly evaluated to form a wrong conclusion such as the one that Re/Code came up with.

WHAT WE KNOW ABOUT SPRINT’S NEXT GENERATION NETWORK

Sprint has been issuing multiple Request for Proposals (and many, many revisions) for its Next Generation Network (NGN) for almost a year now. Previously, Sprint’s Network Vision network plan substantially reduced the size of the equipment at each site and consolidated multiple carriers’ (Sprint, Nextel, and Clearwire) frequencies into one set of equipment. The NGN is an attempt  to densify the Sprint network using a small number of new macrocells, but a significant number of mini-macro small cells. Mini-macro cell sites are smaller than traditional cell tower sites, but larger than small cells.

to densify the Sprint network using a small number of new macrocells, but a significant number of mini-macro small cells. Mini-macro cell sites are smaller than traditional cell tower sites, but larger than small cells.

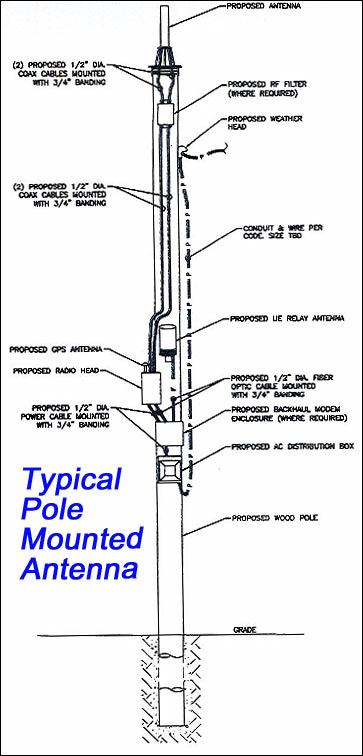

- Sprint has entered into an agreement with Mobilitie to fund and deploy these mini-macro sites like the one shown, at right, that was submitted to Salem City, Mass. on November 6, 2015 (and ultimately rejected by the City). Estimates for the number of mini-macro sites to be deployed are between 50,000 and 70,000. Sprint is using these mini-macro sites to densify their network and to better use their higher frequency spectrum (2.5GHz) acquired from Clearwire which requires denser deployment of cell sites to be effective. When deployed correctly, the higher frequency works great for data.

- Based upon inquiries to our municipal clients, it appears that Mobilitie is targeting government and utility owned property for these mini-macro cell sites. Other attempts by wireless carriers to deploy small cells on private property have demonstrated that while the equipment cost for small cells is significantly less than a large macrocell (or tower site), the site acquisition and routing of power and backhaul is similarly expensive as deploying a macrocell. As a result, we have observed a significant increase in the number of requests being made to the municipalities for lease and use of municipal owned utility structures or placement of new structures or antennas in existing utility right of ways throughout cities. At this point, we are unaware of any actually deployed mini-macro sites. Mobilitie appears to be testing the market and attempting to enter into franchise agreements and master lease agreements with municipalities.

- If Mobilitie and/or Sprint are treated as a utility, in many states they receive the benefit of having federally regulated pole attachment rates to their equipment installation. Furthermore, Mobilitie (and other similar small cell and Distributed Antenna System developers like Crown Castle) often seeks to attempt to convince the local municipality that they can’t be charged traditional lease rates or franchise fees for new poles. The reason is that the federal pole attachment rates are often pennies on the dollar as compared to what they would be charged otherwise by these same utilities or municipalities. Furthermore, by using existing poles, small cell providers avoid some, but not all of the difficult zoning hurdles to erection of new towers.

- We have a few hundred municipal clients across the United States and advise them daily on the appropriate cell tower lease rates they should be charging for macrocell leases. Lease rates for macrocell towers and cell sites on rooftops and water towers on governmental property in urban and suburban areas are typically 25% or more higher than those for commensurate private property. The only places where lease rates are less than private leases are in large federal agencies with large rural land holdings such as the Bureau of Land Management, the National Park Service, and the National Forest Service. However, with those entities, lease negotiations take years and there are substantial environmental hurdles that have to be met before a lease is approved.

- Crown Castle and American Tower have long term tenant leases in place with carriers including Sprint. The average tenant lease between the carriers and the tower companies and the wireless carriers have on average between 7 and 8 years remaining before the tenants can terminate. This means that Sprint likely cannot terminate its leases with Crown Castle and American Tower for 7-8 years. (We don’t know the specific remaining term on the Sprint/Crown Castle or Sprint/American Tower master lease agreements).

- Sprint technically still owns the 6,600 towers they sold to Crown Castle in 2007 (via an intermediary Global Signal). Crown Castle is subleasing those towers from Sprint under a pre-paid capitalized sublease agreement. Those sites are also subject to a master lease agreement with defined lease rates that are fair, in our opinion. American Tower acquired 2,000 towers from SpectraSite who also acquired the tower from Nextel via a pre-paid capitalized lease agreement and as such, Sprint still owns those towers as well.

- Sprint has on multiple occasions issued Requests for Proposals (RFP) to all tower companies that identify a list of Sprint sites where the ground lease or the collocation lease for the tower or cell site are costly. (As have other wireless carriers like AT&T.) Sprint requests in the RFP that those tower companies with an interest in building alternative sites/towers next to the problematic sites propose lease terms for Sprint. Sprint would enter into a Build to Suit agreement with the winning tower company(s) and move their equipment from the costly tower to the newly built tower. Historically, these RFPs have resulting in only a very small percentage (>5%) to actually be relocated. More likely in our opinion, these RFPs are generated specifically to encourage negotiation on master lease agreements with the large tower companies and are not intended to result in the actual relocation of a significant number of macrocell towers.

- Sprint is attempting to use Clearwire spectrum and microwave sites for its backhaul. The 2.5GHz spectrum is effective at transmitting high amounts of data. This will allow Sprint to avoid leasing (to a certain extent) fiber backhaul from AT&T, Verizon, and every other fiber provider from whom provides dark or lit fiber service to Sprint. It is important to recognize though that eventually that the traffic eventually has to connect to the landline network- and often this will be done through fiber.

RE/CODE’S IMPROPER DEDUCTIVE REASONING

Re/code and/or their source appears to be inferring from the limited public information available about the NGN and information from an unknown source that Sprint’s plan includes the relocation of existing collocations from Crown Castle and American Tower in mass to towers built by Mobilitie to government owned properties. We, like Wireless Estimator, believe that Re/code and/or their sources came to this conclusion improperly. While Mobilitie and Sprint are seeking to develop mini-macros on governmental land and utility structures, they are not going to terminate thousands or even hundreds of existing macro cell collocation leases with American Tower and Crown Castle as a result.

The mini-macro cells are complimentary to the macro cells and exist underneath and in-between the macrocells, creating what the industry refers to as a Het-Net or heterogeneous network. In a Het-Net, both components are equally necessary with the macro cells providing overarching coverage and supporting a significant amount of individual users while the mini-macros providing highly localized data capacity. Consider that it takes 10-30 small cells to replace the coverage of one macrocell. Sprint isn’t deploying mini-macros to terminate existing macrocell leases, they are deploying them to add capacity to their existing macros. They are certainly targeting governmental properties which are commensurately cheaper in states that have chosen to adhere to federal pole attachment regulations and rates. For those states that haven’t, there isn’t a significant cost advantage.

Sprint and Mobilitie may choose to use small cells/mini-macros to reduce the number of new collocations on existing American Tower, Crown Castle, and SBAC towers in urban and densely populated suburban areas where mini-macros make fiscal sense. However, in rural areas and sparely populated suburban areas, collocations on existing cell towers are too cost efficient and Sprint will continue to keep their collocation leases on such towers. In other words, the Sprint NGN plan will reduce the number of new inbound collocation leases on macrocell towers like those owned by Crown Castle and American Tower, but by and far between, this won’t contribute to a wholesale move by Sprint from American Tower and Crown Castle towers to Mobilitie owned and developed macrocell towers on governmental property.

As it pertains to existing collocations on American Tower and Crown Castle towers, Sprint is under master leases with both companies that likely limit their ability to leave the towers and it is our strong opinion that Sprint is not that incentivized on a wide basis to do so. There will be cases where Sprint (and other carriers) will opportunistically use small cells to reduce their dependence upon some of their more expensive leases. However, the cost of relocating from one site to another is substantial ($100,000+) and the burden of getting zoning approval for a new tower near an existing one in most urban and suburban markets is difficult. Local municipalities push hard against proliferation of towers especially when there are existing towers that have structural capacity for the intended user of the new tower.

OUR READ ABOUT SPRINT’S NEXT GENERATION NETWORK

- There will not be a mass migration/termination from AMT and CCI towers for existing collocations by Sprint. At worst, there may be opportunistic terminations by Sprint on a few hundred towers as Sprint attempts to demonstrate a show of force in their negotiations on upcoming master leases. However, with 20,000 to 30,000 leases on the public tower company towers, Sprint is still beholden to the public tower companies whether they like it or not. Any effort to abandon a significant amount of towers with AMT, CCI, or SBAC will result in increased pricing pressure on the remaining leases. Like it or not, Sprint is beholden to the public tower companies just as the tower companies are beholden to Sprint.

- Sprint and Mobilitie will continue to build mini-macros on governmental property or utility right of ways. These sites will be cheaper than those on private property or on the public tower company’s towers. CCI probably has more to lose than AMT or SBAC in this regard due to their substantially bigger interest and investment in small cells. We are seeing specific instances where both CCI and Mobilitie are actively courting our municipalities to gain access to municipal rights of way and structures.

- We wonder whether sources from Sprint planted this story with Re/Code or gave them enough information such that Re/Code’s author jumped to the wrong conclusions. Sprint’s unwillingness to confirm or deny this story is expected. The decrease to the tower company market caps certainly helps Sprint in pending master lease negotiations.

OUR CONCLUSION AND RECOMMENDATIONS

Unless Re/code and its sources can provide more documentation of the specifics of this plan, this story by Re/code seems to be more harmful than helpful and demonstrates what poor inductive reasoning can do. While we aren’t that optimistic that Sprint’s Next Generation Network will reverse Sprint’s fortunes, we also don’t see that the almost 10% drop in value was warranted from the Re/code unconfirmed reporting. If you were bullish on Sprint before, you should be even more so now.

About the author: Ken Schmidt is recognized as the foremost cell tower lease consultant in the country. He is the owner and founder of Steel in the Air, Inc. Steel in the Air assists public and private landowners and structure owners with negotiating cell tower leases.

About the author: Ken Schmidt is recognized as the foremost cell tower lease consultant in the country. He is the owner and founder of Steel in the Air, Inc. Steel in the Air assists public and private landowners and structure owners with negotiating cell tower leases.