When Wireless Estimator first reported that Verizon was failing to honor its commitments under the NATE framework agreement brokered by the FCC as a condition of its $20 billion acquisition of Frontier Communications, the story gained immediate traction — picked up by industry media, beltway subscription alerts, and outlets reaching deep into telecom policy circles.

Verizon’s spokesman, Rich Young, offered a carefully worded response to Politico: “We take our commitments to the NATE framework seriously and are confident in our compliance with its terms. We look forward to continuing our good-faith partnership with NATE as we work together to implement the agreement.”

That statement is difficult to sustain in light of the evidence. Across every market reviewed, Verizon imposed pricing reductions on contractors rather than the inflation adjustments it committed to — a fact that requires no internal documentation to establish. That documentation, however, exists and has been reviewed by Wireless Estimator.

The RFP process is effectively complete across most markets. Contractors have received notifications. The results are in. And what those results show is not a company that took its commitments seriously. What they show is a company that structured a process designed from the beginning to arrive at a predetermined outcome — lower prices, fewer contractors, and a consolidation model that the framework agreement explicitly prohibited — while managing appearances carefully enough to avoid regulatory consequences.

That calculation may now be running out of runway.

What Verizon Promised

The commitments Verizon made to the FCC in connection with the Frontier merger approval are documented in a formal letter signed by Verizon’s Senior Vice President and Deputy General Counsel, submitted to the FCC Secretary on May 15, 2025, under WC Docket No. 24-445.

They are specific and enforceable. Verizon committed to instituting a region-based RFP process, aligned with its matrix pricing structure, to allow vendors to account for inflation. It is committed to transparency in the bidding process, including making the methodology of its annual pricing review available to NATE members. It committed explicitly not to use turf vendor models — subject to details to be discussed in working group meetings. And it committed to conducting an annual review of the pricing matrix to evaluate whether macro-economic adjustments are warranted.

Every one of those commitments has been broken. Not bent. Not interpreted creatively. Broken.

The CEO Mandate Behind the Curtain

To understand why Verizon’s Ireland-based team has been pressing contractors to accept pricing below 2021 rates, it helps to understand what is motivating the people at the top of the organization, giving them direction.

Dan Schulman became Verizon’s CEO in October 2025, inheriting a company that had suffered five consecutive years of market share losses. His mandate from the board was unambiguous: cut costs, cut headcount, and restore shareholder value. He delivered immediately — 13,000 layoffs in Q4 2025, the largest workforce reduction in Verizon’s history, followed by a commitment to $5 billion in operating expense savings by the end of 2026 and a capex reduction to $16 to $16.5 billion for the year, a combined $4 billion reduction from the prior Verizon and Frontier combined run rate.

Schulman’s compensation is directly tied to delivering those results. His total reported 2025 compensation was $34.3 million. His long-term incentive package includes a $30 million performance share unit grant that vests based on total shareholder return through the end of 2027, and a supplemental grant of 222,222 PSUs that can pay out at up to 300% of target based on Verizon’s share price reaching between $55 and $75 by the end of 2028. In plain terms, every dollar Schulman cuts from the cost structure between now and 2028 has a direct and meaningful impact on his personal compensation.

Tower construction contracts are a component of that cost structure. The Ireland-based operations team managing U.S. contractor pricing did not invent the drive to reduce rates out of institutional habit. They received a mandate from leadership to reduce costs aggressively and across every category. Contractor pricing was not exempt. When Schulman told investors Verizon was pursuing “contract renegotiations” as part of its $5 billion savings target, the tower-construction contractors bidding on regional RFPs were included in that math. The framework agreement commitments made to the FCC in May 2025 were, by October 2025, competing directly with a new CEO’s financial incentive to cut every cost in sight. The contractors lost that competition.

The Pricing Betrayal

The commitment Verizon made to the FCC — to institute a regional RFP process that allows vendors to account for inflation — has not been honored in any market that Wireless Estimator has reviewed. Not a single market shows a net price increase for contractors. In some cases, Verizon offered modest gains of three or four percent in one work category while simultaneously reducing percentages in another, ensuring that the net result — across all segments combined — remained negative. Contractors absorbed the losses. Schulman counted the savings.

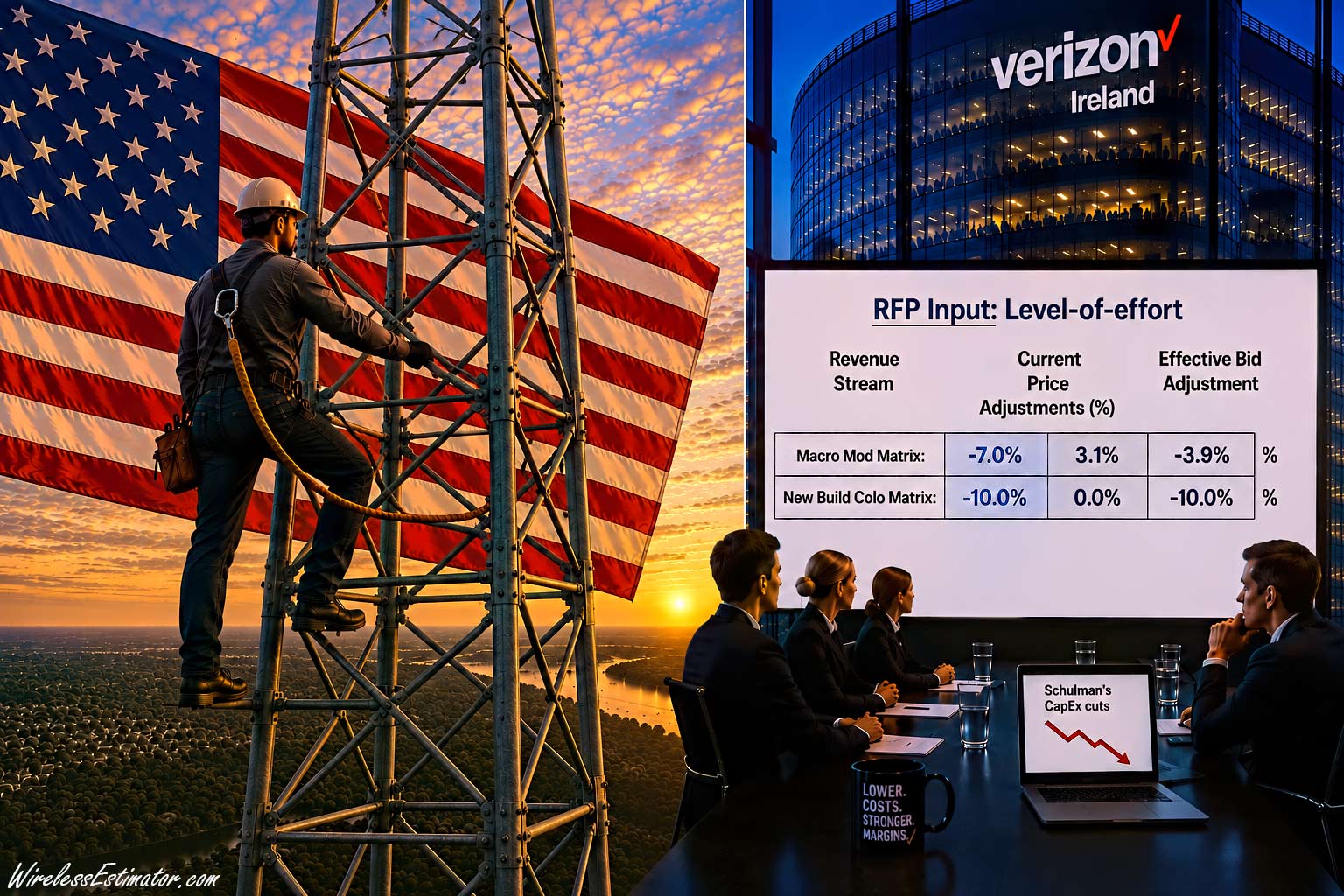

Bid sheets reviewed by Wireless Estimator from two geographically separate markets — one on the East Coast and one on the West Coast — illustrate both the regional variation in Verizon’s approach and the consistency of its ultimate outcome. In the East Coast market, contractors were asked to bid a 7% reduction on Macro Modifications and 10% on New Build Colocation. After accounting for an existing 3.1% price adjustment already embedded in the current matrix, the effective bid landed at minus 3.9% on Macro Mods and minus 10% on New Build Colo. In the West Coast market, the RFP input sought a 6% reduction on Macro Modifications and 4% on New Build Colocation. With the same 3.1% existing adjustment applied, the effective outcome was minus 2.9% on Macro Mods and minus 4% on New Build Colo.

The numbers differ by market. The direction does not. In both cases — on opposite ends of the country, in markets with different labor costs, geographic challenges, and operational realities — the result was a net reduction relative to the 2021 pricing baseline, which was supposed to have been adjusted upward for inflation. Verizon did not deliver regional pricing that reflected regional conditions. It delivered uniform reductions dressed in regional packaging.

Verizon’s letter to the FCC also committed to conducting an annual review of the pricing matrix to evaluate whether macro-economic adjustments are warranted. While insufficient time has passed since the current bids were submitted to trigger a formal annual review, the trajectory of those bids makes the value of any such review questionable. A review process controlled entirely by Verizon — with no binding mechanism to ensure the results serve contractor interests rather than the carrier’s capex reduction targets — offers little assurance that the outcome would differ from what the RFP process has already produced.

Verizon Will Claim It Raised Prices. The Bid Sheet Tells a Different Story.

Verizon did make upward adjustments to portions of its pricing matrix before the RFP opened — and it will almost certainly cite those adjustments as evidence of good-faith compliance with the inflation accommodation commitment it made to the FCC. That defense crumbles under examination. The adjustments were made to a matrix that Verizon controls, were not independently verified, and in at least two markets, a pre-existing 10% regional premium was already in place before the bidding began.

None of it was new money. And none of it survived contact with the bid sheet — because the same document that showed those adjustments asked contractors to bid them back down. Verizon built itself a defense that will not stand up. And it didn’t build contractors a raise.

When NATE CEO Todd Schlekeway told Politico that “Verizon’s pricing model remains unsustainable and hasn’t kept pace with inflation since 2021,” he was understating the situation. Verizon didn’t merely fail to keep pace with inflation. It moved in the opposite direction, fully aware of the regulatory scrutiny it was operating under. That awareness is documented in Verizon’s own words.

A Process Designed Around Regulatory Optics

Internal Verizon communications, reviewed by Wireless Estimator, reveal that in at least one major market, Verizon’s team was actively discussing how to structure the RFP award not based on what made operational sense, but on what would withstand FCC scrutiny. The concern about “legal oversight and FCC contention” was explicitly cited as a factor in determining how many preferred suppliers to select and how to close the award.

This is not compliance. This is the management of appearances. The framework commitments Verizon made to the FCC weren’t being honored — they were being engineered around.

What Verizon described publicly as a transparent regional bidding process was, internally, a managed outcome. These awards are being directed by Verizon’s Ireland-based operations team, which has been coordinating U.S. contractor pricing decisions. The people setting the rates for American tower construction crews are doing so from Dublin — under a CEO mandate to cut costs — with limited understanding of or apparent concern for the operational realities those crews face in the field.

Long-Term Contractors Left Behind

In Indiana, a contractor that had performed between 25% and 35% of Verizon’s regional work for 12 consecutive years bid on the new RFP, did not make the cut, and received no explanation when one was requested. That company could close within months if alternative work cannot be found.

Approximately 18 employees face losing their jobs, some depending on the company’s health insurance for cancer treatments and other serious ongoing medical needs.

Wireless Estimator is aware that this is far from an isolated case. Contractors, both large and small, across numerous markets, are facing the same situation — excluded or passed over without transparency, left to absorb the consequences of a process that Verizon’s own internal discussions show was structured around regulatory optics rather than fair competition. The impact will extend well beyond the companies directly affected. The entire contracting and supplier ecosystem — the crews, the vendors, the trainers, the communities — will feel it. The Indiana contractor is not an outlier. It is a preview.

These companies built Verizon’s network for decades. They received no explanation for their exclusion. The likely reason is straightforward — they were unwilling to sign contracts at rates that would have forced them out of business anyway. Verizon simply accelerated the timeline.

In other markets, established contractors with years of regional history report not being invited to bid at all. In markets where up to 20 or more companies were brought in to create the appearance of a competitive process, long-tenured regional contractors were, in some cases, bypassed entirely in favor of out-of-region participants who, some sources suggest, were never realistic candidates for the work. The practical effect was to manufacture a pricing floor through the weight of bidder volume rather than genuine regional market competition — a reverse auction in all but name.

One senior industry voice put the pattern in historical terms that the FCC would do well to consider. What Verizon is doing to its contractor base, he argued, is not a negotiating posture. It is a consolidation strategy of the kind not seen since the Rockefeller and Morgan era — when the federal government ultimately concluded that the market alone could not correct what dominant corporate interests had deliberately engineered. “We do need a heavy hand to stop what is going on,” he said. History, he noted, shows what happens when that hand arrives too late.

The human cost of Verizon’s approach is not abstract. Another key contractor expressed a concern shared broadly across the industry: “I fear the Verizon plan will put more contractors out of business than any other episode of the past in tower contracting. They will be replaced with big contractors and fly-by-night small guys.”

Questions For Verizon

Several questions need to be asked of Verizon that go to the heart of whether the commitments it made to the FCC have any practical effect. These questions reflect the documented gaps between what the carrier promised and what the RFP process has delivered.

The first question concerns the composition of the bidder pool in each region — specifically, whether the companies invited to bid were genuinely regional contractors capable of performing the work, or whether out-of-region participants were included in a manner that effectively undermines the agreement’s regional pricing intent.

The second inquiry addresses which contractors were ultimately awarded work in each region and whether the resulting allocation reflects the competitive, non-turf model Verizon committed to — or a concentrated preferred-supplier structure described in its own internal documents.

The answer in at least some markets is already revealing. Ericsson, primarily an equipment supplier, has been selected as a preferred supplier despite Verizon’s knowledge that the company lacks dedicated crews to perform construction work. Ericsson shut down its entire U.S. field services operation effective October 1, 2023, laying off approximately 750 employees and citing a downturn in market demand. All construction work was transitioned to external providers at that time.

Verizon awarded Ericsson preferred supplier status with full knowledge of this. Without an in-house workforce, Ericsson will be compelled to subcontract the work it has been awarded. That subcontract market is precisely where illegal 1099 misclassification is most prevalent, where worker protections are thinnest, and where the safety and quality standards Verizon committed to reinforcing are most at risk of being abandoned. Verizon is committed specifically to limiting 1099 crew use to narrow, pre-approved circumstances. Pushing work into a subcontract chain with limited oversight is not consistent with that commitment.

A third question concerns the final matrix pricing outcome in each region. If the answer across every market is zero adjustment or a net reduction from 2021 rates — which Wireless Estimator’s research indicates is precisely the case — Verizon will need to explain to both NATE and the FCC how that outcome satisfies its explicit commitment to allow vendors to account for inflation.

A fourth question should require Verizon to address its treatment of long-standing regional contractors — specifically, what criteria were used to determine which contractors were invited to participate, and what recourse, if any, exists for established vendors who were excluded from markets they had served for years without explanation.

If Verizon is unable or unwilling to provide satisfactory answers to any of these questions, the record of non-compliance becomes that much harder to dismiss.

Chairman Carr: The Evidence Is Now in Front of You

When Wireless Estimator’s original reporting reached FCC Chairman Brendan Carr, he responded on X: “If Verizon is not living up to their commitments, then that would be a problem.” The reporting gave him a conditional. The evidence now removes the condition.

Chairman Carr told Politico in April that the FCC was “monitoring” the situation and hoped it would “land in a good spot that works for everybody.” With RFP awards now finalized across most markets, the landing has occurred. It did not land in a good spot for the contractors who built Verizon’s network. It landed where Verizon’s internal teams designed it to land — at discounts off five-year-old rates, with the majority of work concentrated in a handful of preferred suppliers, and long-term regional contractors forced out without explanation.

The commitments Verizon made to the FCC in May 2025 were a condition of one of the largest telecom mergers in history. They are not aspirational targets to be honored when convenient and ignored when a new CEO arrives with a mandate to cut $5 billion in costs. They are commitments. Verizon accepted them. Verizon’s own internal communications show that its teams were more focused on managing FCC optics than on fulfilling those commitments in good faith.

Chairman Carr now has the evidence. He has the signed letter of commitment Verizon submitted to the FCC. He has documented pricing outcomes showing zero inflation accommodation across every market reviewed. He has accounts of long-term contractors excluded from markets they built, without explanation. He has NATE’s unambiguous statement that the parties are “miles apart” on how the commitments should be implemented. And he has internal Verizon discussions that explicitly cite FCC scrutiny as a factor in structuring award decisions. What he does not yet have is a record of having acted on any of it.

The framework commitments give the FCC both the authority and the roadmap to intervene. The following actions would give Verizon clear direction on what compliance actually requires — and give the FCC a documented basis for enforcement that goes beyond monitoring.

What the FCC Should Do

The FCC should demand full transparency documentation on the RFP process. Verizon’s letter to the FCC commits explicitly to transparency, including making the methodology of its pricing review available to NATE members. The FCC should require Verizon to produce its full means and methods for each regional RFP — who was invited, how the bidder pool was constructed, how awards were determined, and what criteria were applied. A process structured around managing FCC optics is not transparent.

Require that compensation reflect inflation. Verizon is committed to a regional RFP process that allows vendors to account for inflation and to annual macro-economic pricing reviews. The FCC should benchmark that commitment against objective measures — the Davis-Bacon Act wage determinations and Bureau of Labor Statistics construction wage data both provide defensible, independent standards. By either measure, construction labor costs have increased substantially since 2021. Verizon’s pricing has moved in the opposite direction. What makes this particularly consequential is that the rates being set now are locked for three years — meaning contractors who accept today’s terms are effectively locked into pre-2021 pricing through 2028 or 2029, with no provision for future inflation adjustments. The FCC should require that any multi-year agreement include an inflation escalator tied to an objective index.

Demand answers on the use of contractors without self-performing capability. Verizon committed not to use turf vendor models. It will argue that it is using five or more vendors per region and therefore is not concentrating work inappropriately. That argument is technically defensible, but it runs counter to the spirit of what was committed to. Awarding preferred supplier status to companies that cannot self-perform the work — and that will push it into a subcontract chain with limited oversight — does not produce the healthy, competitive regional contractor ecosystem the commitment was designed to protect.

Ericsson is not an exception. It is an example. Wireless Estimator is aware of multiple contractors selected across Verizon sub-markets who are unable to self-perform the work they will be awarded. Every one of those awards pushes Verizon construction work deeper into a subcontract chain that the FCC cannot see, that Verizon has limited ability to police, and where the workforce commitments made in the May 2025 letter to the FCC exist only on paper.

Require a full accounting of the reverse auction process. The contractors who accepted Verizon’s pricing did so under conditions that cannot reasonably be characterized as free and competitive negotiation. Brought into a process that invited dozens of bidders — many with no realistic capability to perform the work — they faced take-it-or-leave-it pricing offers with zero transparency into how bids were being evaluated. Agreements reached under those conditions, with closure as the only alternative, reflect duress rather than market consensus. The FCC should determine whether rates accepted under those conditions can be treated as a valid market outcome for purposes of Verizon’s commitments.

The monitoring phase is over. The industry is watching. The contractors who built Verizon’s network are closing their doors. The FCC has the authority, the evidence, and the roadmap. The only remaining question is whether it will act.

Monopsony: The Word That Explains Everything

The mechanism that made all of this possible has a name that rarely appears in trade press coverage of tower construction pricing disputes, but deserves to be stated plainly: monopsony. Verizon, along with AT&T and T-Mobile, exercises buyer-side market dominance over the contractor ecosystem. There is no competitive marketplace to which a displaced tower contractor can redirect their workforce and equipment. There are three carriers, all pursuing the same pricing strategy simultaneously, which means the theoretical option to walk away from Verizon’s terms is, for most contractors, no option at all. That structural reality is what enabled Dublin to dictate rates from across the Atlantic, made the RFP process susceptible to manipulation, made take-it-or-leave-it offers credible, and ultimately led contractors to accept negative pricing off a 2021 baseline after years of frozen rates.

The FCC framework agreement was, in effect, the only external constraint on that monopsony power. Violating it is not merely a breach of a negotiated commitment. It is the removal of the only check the contractor market had.

If regulatory intervention fails to produce meaningful relief, legal observers note that a coordinated antitrust lawsuit against the carriers — examining whether three companies pursuing identical pricing strategies constitute unlawful monopsony — may be the industry’s last available remedy.